The Limitation of Liability Clause: How to Cap Your Risk Before You Sign

A limitation of liability clause caps the maximum amount one party can recover from another if a contract goes wrong — and without one, your financial exposure is potentially unlimited. This clause is the single most negotiated term in commercial contracts, according to World Commerce & Contracting's annual survey of over 2,000 agreements. For freelancers, small business owners, and landlords, getting this clause right is the difference between a manageable setback and a lawsuit that threatens the business itself.

The core mechanics are straightforward: the clause sets a dollar ceiling on damages, typically excludes certain damage types (like lost profits), and may carve out exceptions for specific breaches (like confidentiality violations or IP infringement). The complexity — and the risk — lies in the details.

Why Contracts Without a Limitation of Liability Clause Are Dangerous

Without a liability cap, the default rule in most U.S. jurisdictions is that the breaching party owes whatever damages flow naturally from the breach — a standard established in Hadley v. Baxendale (1854) and still applied in American courts today. That includes direct damages (the cost to fix the problem) and, in many cases, consequential damages (the downstream financial losses the breach caused).

A practical example: You're a freelance web developer. You build a client's e-commerce site. A bug in the checkout flow causes the site to go down for 48 hours during a holiday sale. Direct damages might be $5,000 (the cost to fix the bug and restore the site). Consequential damages could be $200,000+ (the revenue the client lost during the outage, plus customer acquisition costs to replace churned buyers). Without a liability cap, you're exposed to the full amount — potentially 40× your project fee.

The same math applies to landlords (a maintenance failure that causes tenant business losses), consultants (a recommendation that leads to a bad investment), and any service provider whose work touches the client's revenue stream.

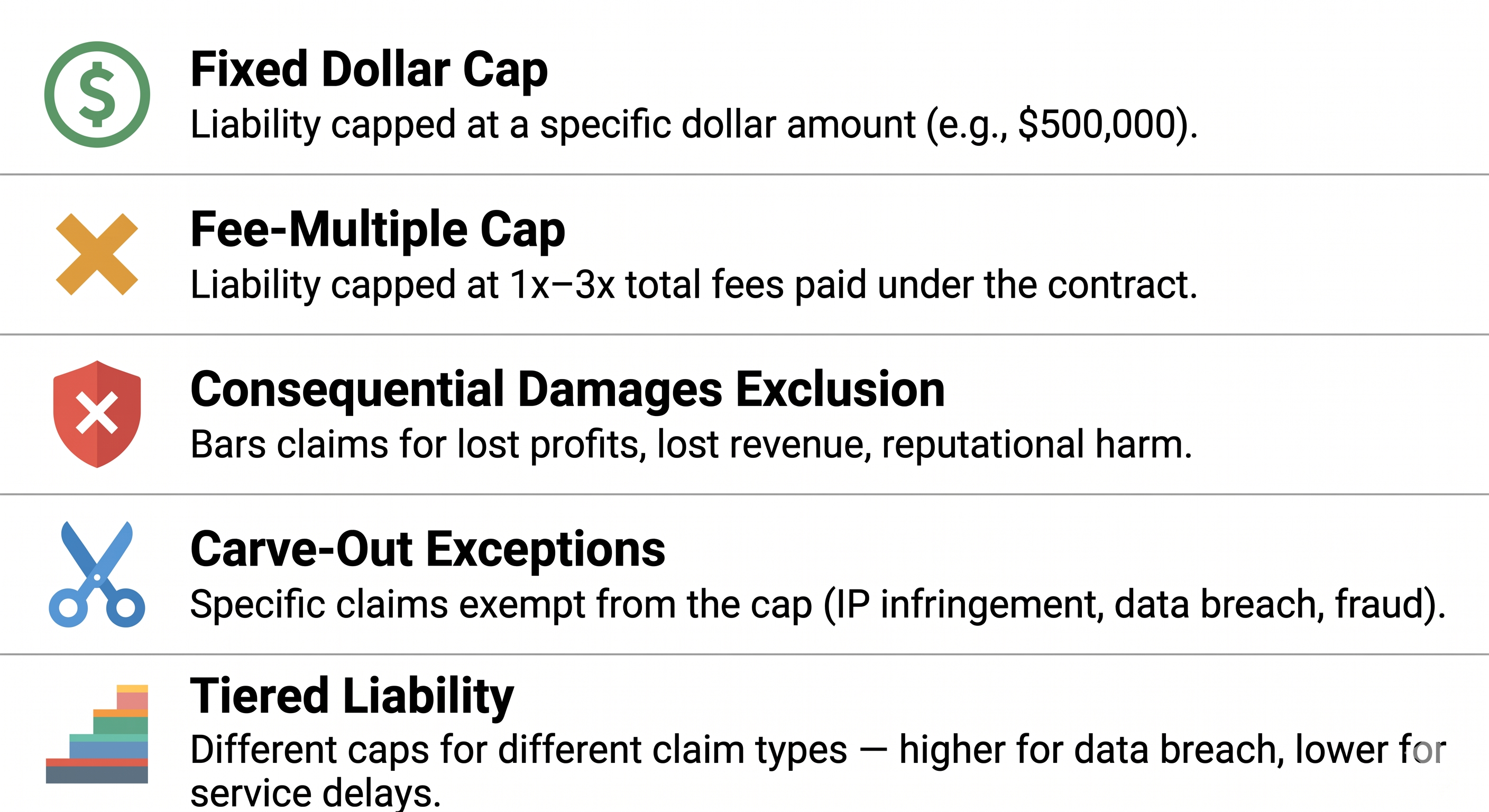

Types of Limitation of Liability Clauses

Liability caps come in five structural forms. Each distributes risk differently between the parties.

1. Fixed Dollar Cap

The simplest form: "Neither party's total liability shall exceed $50,000." Both sides know the maximum exposure from day one. Works best for fixed-scope projects where the risk is predictable.

Drawback: If a $50,000 cap sits on a $500,000 contract, the cap may be too low to meaningfully compensate the injured party — and courts in some jurisdictions may find it unconscionable.

2. Fee-Multiple Cap

"Liability shall not exceed [X] times the total fees paid under this Agreement." This is the most common structure in SaaS contracts, consulting agreements, and professional services.

Typical multiples by contract type:

| Contract Type | Typical Cap Multiple | Why |

|---|---|---|

| SaaS subscription | 12 months of fees paid | Recurring revenue; risk scales with usage duration |

| Consulting/professional services | 1–2× total project fees | Bounded scope; risk is proportional to engagement size |

| Freelance creative work | 1× total fees paid | Low-margin work; higher multiples make the project unprofitable |

| Commercial lease | Security deposit + 3 months rent | Landlord's exposure limited to occupancy-related losses |

| NDA / confidentiality agreement | 2–5× fees or a fixed dollar amount | Information breaches cause outsized damages relative to contract value |

| Construction / physical work | 1–2× contract value | Physical damage liability can be significant; insurance carries the rest |

The Liability Cap Calculator: To determine whether a proposed cap is reasonable, divide the cap by your maximum realistic downside. If a client's worst-case loss from your breach is $100,000 and the cap is set at $10,000 (your fee), the client bears 90% of the risk. If the cap is $200,000, you bear the excess. Neither party should accept a cap that creates moral hazard — a cap so low the other side has no financial incentive to perform.

3. Consequential Damages Exclusion

Rather than capping total liability, this form excludes specific damage types: "Neither party shall be liable for lost profits, loss of business, loss of data, or any indirect, incidental, special, or consequential damages." The party can still recover direct damages (the cost to fix the breach), but not the downstream financial impact.

This is the most common limitation in technology contracts. Cornell Law Institute defines consequential damages as losses that don't flow directly from the breach but result from special circumstances — like a delivery company's truck breaking down, which delays a time-sensitive shipment, which causes the buyer to lose a separate contract.

Red flag: Mutual consequential damages exclusions look fair but may not be. If you're a small service provider and your client is a large company, you're unlikely to suffer consequential damages from their breach (they'll just not pay you). But they could suffer significant consequential damages from yours. A mutual exclusion disproportionately protects you — which means sophisticated counterparties will push back on it.

4. Carve-Out Exceptions

Most limitation of liability clauses include exceptions — categories of breach where the cap doesn't apply. Common carve-outs:

- Confidentiality / data breach — damages from leaking proprietary information are hard to quantify in advance, so they're often excluded from caps

- IP infringement — if your work infringes a third party's intellectual property, the cap doesn't protect you

- Gross negligence or willful misconduct — caps only protect against ordinary negligence, not intentional harm

- Indemnification obligations — if you've agreed to indemnify the other party against third-party claims, those obligations sit outside the cap

Negotiation point: The more carve-outs, the less the cap actually protects you. If a clause caps liability at $50,000 but carves out confidentiality, IP, indemnification, and willful misconduct, the cap only applies to a narrow band of ordinary performance failures. Negotiate carve-outs as aggressively as you negotiate the cap number itself.

5. Tiered Liability Caps

Advanced agreements use different caps for different breach types. Example: general performance failures capped at 1× fees paid; data breach liability capped at 3× fees paid; IP infringement uncapped. This structure matches risk magnitude to cap size rather than applying a single ceiling across all breach types.

How to Negotiate a Limitation of Liability Clause

When You're the Service Provider (Protecting Yourself)

Start with a 1× fee cap. For freelancer contracts, a cap equal to total fees paid is industry standard. Your client may push for 2× or 3×; anything beyond 3× should trigger a conversation about whether the project economics still work for you.

Insist on a mutual consequential damages exclusion. This is the single highest-value clause for service providers. Without it, a $10,000 project can generate $500,000+ in consequential damage claims if something goes wrong.

Push back on unlimited carve-outs. If the client wants uncapped liability for data breaches, counter with a higher but still capped amount — 3× or 5× fees — rather than unlimited exposure. An uncapped carve-out on a common breach category effectively eliminates the protection the cap provides.

Verify the clause survives termination. A liability clause that expires when the contract ends leaves you exposed for claims filed after the engagement is over. The clause should state it "survives termination of this Agreement."

When You're the Client (Protecting Your Investment)

Don't accept a cap below your realistic downside. If a vendor's breach could cost you $200,000 in lost revenue, a $15,000 liability cap means you're self-insuring the other $185,000. That's a business decision, not a legal one — make it consciously.

Require carve-outs for the breaches that matter most. Confidentiality breaches, data security incidents, and IP infringement should have higher caps or be excluded from the limitation entirely.

Add a severability clause alongside the liability cap. If a court strikes the liability cap as unconscionable, a severability provision preserves the rest of the contract instead of voiding the entire agreement.

Limitation of Liability Clauses and Related Contract Provisions

The liability cap doesn't operate in isolation. Three other clauses interact with it directly:

Indemnification. An indemnification clause requires one party to cover losses from specific events (like third-party IP claims). If the indemnification obligation sits outside the liability cap — which is common — the cap provides less protection than it appears. Always check whether indemnification is subject to the cap or carved out.

Force majeure. A force majeure clause excuses performance during extraordinary events (natural disasters, pandemics, government orders). If a force majeure event triggers a breach, does the liability cap apply to the resulting damages? Most contracts say yes, but confirm.

Insurance requirements. Many commercial contracts require vendors to maintain professional liability (E&O) insurance at specified coverage levels — $1M or $2M is typical. The insurance coverage effectively becomes a second liability cap. If your contractual cap is $50,000 but your insurance covers $1M, your total exposure depends on what the insurance actually covers and what's excluded.

When a liability dispute actually materializes, the contract's dispute resolution mechanism — whether arbitration versus mediation — determines the process and cost of enforcement.

Frequently Asked Questions

About Vladimir Kuzin

Founder & CEO, Shepherdstack LLC

Vlad Kuzin is the founder of Shepherdstack LLC and creator of Pact, an AI-powered contract review tool. He builds software that helps individuals and small businesses understand the documents they sign.

Disclosure: Founder of Shepherdstack LLC, the company behind Pact. All comparison articles use a standardized evaluation methodology applied equally to all tools, including Pact.